🇺🇸 1 Boston Place, Suite 2600, MA 02108

🇬🇧 2 Pear Tree Court, London EC1R 0DS

© 2026, Juro. All rights reserved.

🇺🇸 22 Boston Wharf Rd, Boston, MA 02210

🇬🇧 2 Pear Tree Court, London EC1R 0DS

© 2026, Juro. All rights reserved.

Contract due diligence is the process by which investors and their legal advisers review a company's contracts before completing an investment.

The goal is to understand the commercial, legal, and operational risks embedded in the company's agreements – and to assess whether those risks are acceptable, manageable, or serious enough to affect deal terms.

For finance teams, contract due diligence has a direct impact on deal velocity, valuation, and outcome. Incomplete records, missing signatures, and inconsistent terms don't just create legal complications, they raise questions about how well the business is run.

A clean, well-organised contract repository gives investors confidence and keeps the process moving. So, let's dig into what that looks like in practice, and how your business can make contract due diligence a breeze.

Investors aren't simply checking that contracts exist. They're trying to understand three things: what obligations the business has taken on, what risks those obligations create, and whether the business has managed its contracts with sufficient rigour. The specific focus shifts depending on the stage of the round.

At Series A, investors are typically focused on foundations. The core questions are: does the business have proper agreements in place with customers, employees, and co-founders? Is intellectual property clearly owned by the company? Are there any side agreements, verbal commitments, or informal arrangements that could create exposure?

Many early-stage businesses reach Series A with contracts that were put together quickly, without standardized contract templates or proper execution. Investors understand this – but they'll want to see that gaps have been identified and addressed before the round closes.

At later stages, the lens widens considerably.

Investors will want to understand revenue quality: are customer contracts genuinely recurring, and on what terms? What are the renewal rates, and are there any unusual termination rights that could affect future revenue? They'll also scrutinise liability exposure more carefully, and assess whether the business's legal infrastructure has kept pace with its growth.

At growth rounds, contract due diligence often involves specialist advisers running detailed reviews of all material contracts. Any change-of-control provisions – clauses that could be triggered by the investment itself – will be identified and assessed. So will any contracts where the business has taken on unusually onerous obligations.

Across all stages, the consistent themes are completeness and consistency. Gaps and inconsistencies don't necessarily indicate wrongdoing, but they do suggest a business that hasn't been rigorous about managing its obligations, which is itself a risk factor investors take seriously.

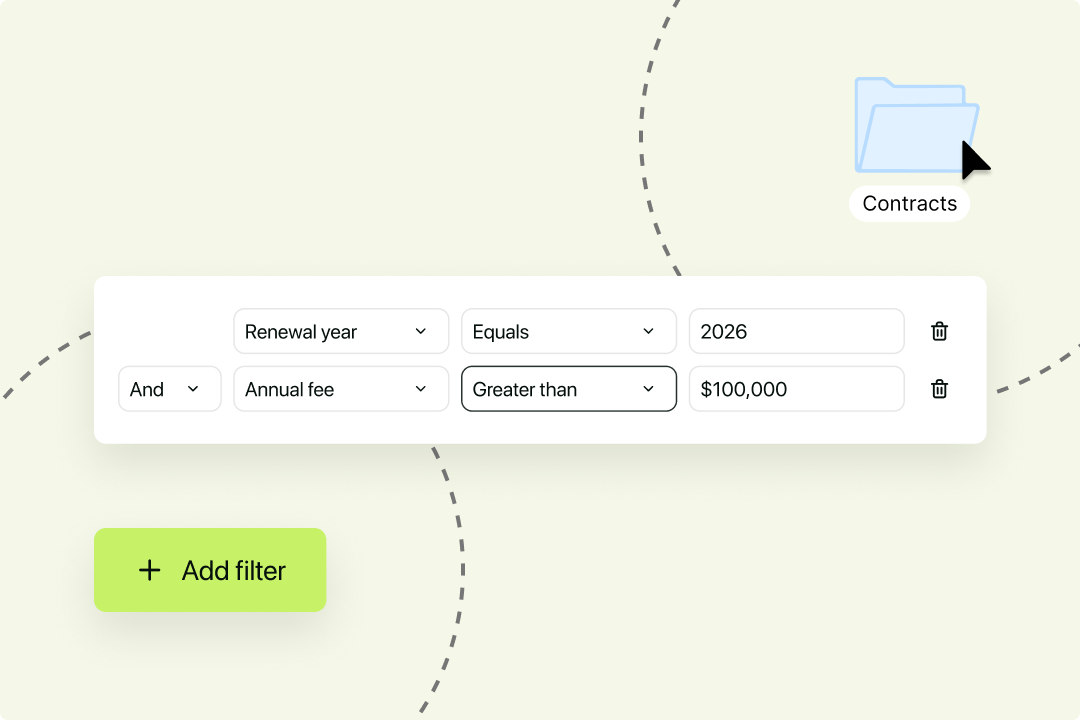

Customer contracts sit at the heart of due diligence for most investors, and the scrutiny intensifies at growth rounds where revenue quality is central to the investment thesis.

Investors will want to understand your standard terms: what liability caps are in place, what the termination rights look like, and whether there are any provisions that could affect revenue predictability.

If your customer contracts vary significantly from deal to deal – because every agreement has been individually negotiated without a consistent baseline – investors will want to understand the range of exposure that creates.

They'll also look closely at renewal mechanics. Are contracts renewing automatically, on what notice, and on what terms?

Auto-renewal contracts can be a positive signal, supporting revenue predictability, or a concern if they've created obligations the business isn't actively tracking.

Investors want confidence that key people are properly contracted. That means written agreements for all employees (not just senior hires) with clear terms covering compensation, equity, notice periods, and post-termination restrictions.

Areas of particular focus include equity arrangements (are option grants properly documented and consistent with the cap table?), garden leave and non-compete provisions for senior roles, and any side agreements or informal commitments not reflected in the main employment contract.

IP ownership is one of the most commonly overlooked areas at early stage, and one of the most consequential. If founders, early employees, or contractors who built core technology didn't formally assign their intellectual property to the company, the business may not own what it believes it owns – which is a fundamental problem for any investor.

Investors will check that IP assignment agreements exist, are properly signed, and cover all work that is material to the business. Gaps here – particularly involving founders or early technical hires – can create significant complications during a fundraise. If you have concerns about IP ownership in your business, take advice from a qualified IP lawyer before diligence begins.

The shareholder agreement governs the relationship between shareholders and sets out rights around voting, share transfers, drag-along, and tag-along provisions.

Investors will review it carefully – both to understand the existing dynamics and to make sure there's nothing that would complicate their investment or a future exit.

If the shareholder agreement hasn't been updated to reflect changes in the cap table since it was originally drafted, that's something to address before diligence starts.

Material supplier contracts – particularly those involving critical infrastructure, exclusivity arrangements, or significant financial commitments – will also come under scrutiny.

Investors want to understand whether the business has supplier dependencies that create concentration risk, and whether there are any unusual terms that could affect operations or costs post-investment.

Understanding what investors flag most often gives you a clear starting point for your pre-diligence review.

Missing or unsigned documents. A contract that was never properly executed isn't enforceable in the way the parties might assume. Missing signatures, particularly on IP assignments and employment agreements, are a recurring issue in early-stage businesses. Often it's because agreements were shared but never formally completed.

Inconsistent terms across the contract portfolio. When different customers, employees, or suppliers are operating under materially different terms, it creates unpredictability. Some variation is inevitable and explainable, but unexplained inconsistencies, or a situation where no two customer contracts look alike, will invite detailed scrutiny.

Poorly defined or unassigned IP ownership. Ambiguity about who owns what is a serious concern. This is particularly common where contractors, agencies, or founders contributed to core IP without a formal assignment in place. If ownership isn't clearly documented, investors will treat it as a risk and may require it to be resolved before the deal can close.

Unusual liability clauses. Uncapped liability provisions, unusual indemnities, or one-sided terms that expose the business to disproportionate risk will attract attention. So will any contracts where the business has given warranties or representations that seem outsized relative to the commercial relationship.

Change-of-control provisions. Some contracts give the counterparty rights to terminate, renegotiate, or require consent in the event of a change of control. Depending on how a deal is structured, an investment can trigger these provisions, and investors will identify all such clauses early in the process.

Untracked autorenewal and key dates. Contracts renewing on unfavourable terms, or expiring at a critical moment, can create real problems. If key dates aren't being actively tracked and managed, it raises questions about contract governance more broadly, and finance teams will be expected to have answers.

A pre-funding contract audit is a structured review of your contract portfolio, conducted before investors begin their own process. The objective is to find and address problems on your own terms, rather than having them surface under time pressure during diligence.

{{quote4}}

Start by locating every contract the business has entered into. That includes customer agreements, supplier contracts, employment agreements, consultant and contractor agreements, IP assignments, shareholder documents, partnership agreements, and any other formal obligations.

If you don't have a clear, complete picture of where all your contracts live, that's the first thing to resolve.

Be thorough. Contracts signed before the current management team arrived, agreements made during periods of rapid hiring, and documents stored in personal email accounts or local drives rather than a central system all count.

If contracts are scattered across multiple tools and inboxes, a central contract repository is the foundation everything else is built on.

Once everything is in one place, organise it by category.

Create a master log that records, for each contract, the counterparty, the contract type, the effective date, the expiry or renewal date, whether it has been properly executed, and any material or unusual terms.

Work through each category with the following questions in mind.

Not everything you find will be equally important. Prioritise issues by materiality: unsigned IP assignments from founders are more urgent than a minor inconsistency in a low-value supplier contract, for example.

For each issue, decide whether it can be addressed before diligence begins, and if so, how. Then, document your findings and the steps taken to address them.

A clear record of your review process is itself a positive signal to investors.

If your review surfaces significant issues around IP ownership, unusual liability, or change-of-control provisions, take advice from qualified legal counsel before diligence begins. Identifying and addressing problems proactively is far better than having them discovered mid-process.

Contract due diligence is a big job, and recruiting help isn't uncommon. Just consider whether a lot of your problems can be solved by a robust contract management system long-term, instead of outsourcing here unnecessarily.

A well-organized data room does two things: it makes due diligence faster, and it signals to investors that the business manages its contracts with rigour. A disorganized data room does the opposite, even if the underlying contracts are sound.

The businesses that find data room preparation straightforward are almost always the ones that were already running a well-structured contract repository before the fundraise began.

When every contract is stored centrally, properly named, and tagged with key contract metadata, building a data room becomes an exercise in sharing what you already have, not a scramble to find and reconstruct it.

Organise your data room by contract category, with a clear and consistent folder structure. Within each folder, use consistent and descriptive file names. Not "NDA v3 FINAL (2)" but "NDA – Acme Corp – Signed – 2023-04-12".

If your contracts live in Juro's repository, they're already stored with structured metadata against each document, so categorising and exporting them for a data room is a matter of filtering and sharing rather than manual sorting.

Include a master index at the top level that maps the structure and lists the key documents in each category.

Investors and their advisers shouldn't have to hunt for anything, and a clear index demonstrates that you know exactly what you have.

Juro's intelligent repository gives you a searchable, filterable view of your entire contract portfolio, which means generating that index, by counterparty, contract type, status, or renewal date, takes minutes rather than hours of spreadsheet work.

If there are contracts with non-standard terms, known gaps, or issues you're aware of, address them in a covering note rather than waiting for them to be discovered. Transparency builds trust; surprises don't.

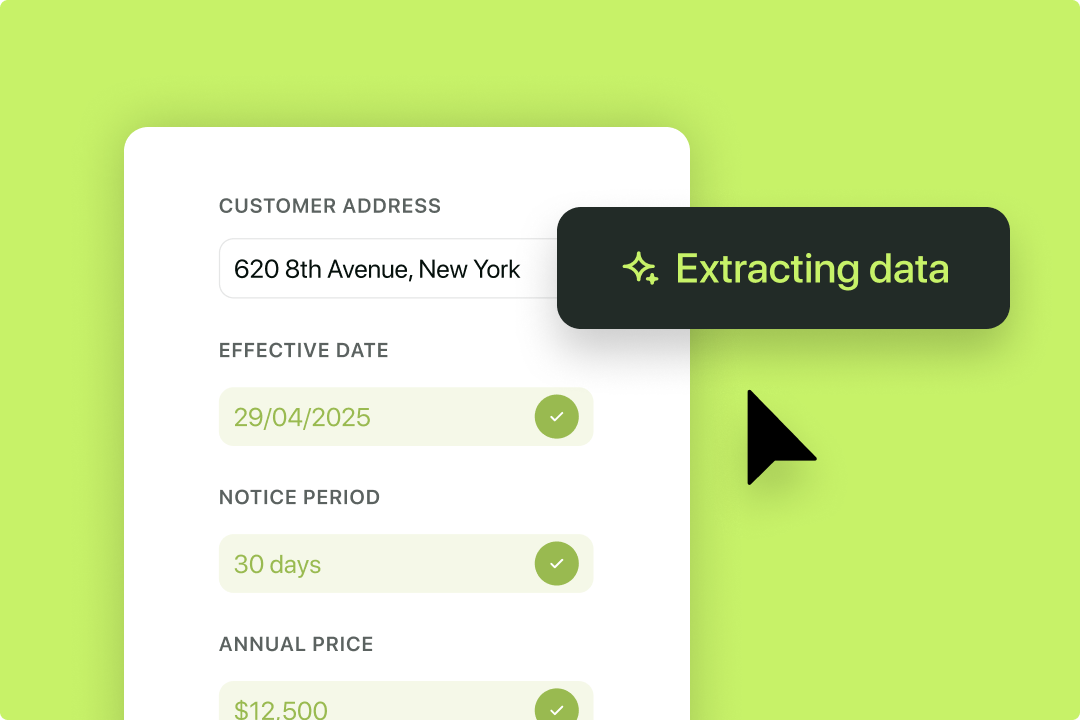

Juro's AI extraction capability can help here too: running an extract across your contract portfolio before diligence begins will surface unusual clauses, missing fields, and data inconsistencies that you can then review and address on your own terms.

Make sure data room access is controlled and auditable. You should know who has accessed what, and be able to revoke access if the deal doesn't proceed. Most virtual data room platforms, including Datasite, Ansarada, and Intralinks, provide this as standard.

Juro's repository maintains a full audit trail on every contract, so if investors or their advisers want to understand the history of a document, who edited it, when it was signed, and what changed between versions, that information is already there.

If there's a gap between when you build the data room and when due diligence actually starts, make sure it reflects your current position.

Updating documents mid-process, or adding material contracts that should have been there from the start, is unsettling for investors and slows everything down. A live repository that your team uses day to day solves this by default: the data room isn't a snapshot you build once and hope stays accurate, it's a reflection of a system that's always up to date.

This checklist covers the issues that come up most frequently in pre-investment contract reviews. It isn't exhaustive, and it isn't a substitute for qualified legal advice, but it's a practical starting point for any finance team preparing for a fundraise.

Most businesses treat contract due diligence as a pre-round fire drill, scrambling to locate documents, chase signatures, and piece together a picture of their obligations under time pressure. It's stressful, it's slow, and it almost always surfaces problems that would have been straightforward to address earlier.

The businesses that go through due diligence most smoothly are the ones that maintained good contract hygiene throughout. That means a complete, searchable repository updated as a matter of course, key dates tracked proactively, and consistent templates with a clear record of any deviations.

For finance teams, the value extends well beyond fundraising. Knowing when contracts renew, understanding liability exposure across the full book of agreements, and being able to report on contract obligations without manual assembly are everyday capabilities. The finance teams best placed when investors come knocking are the ones that don't have to change how they work to get ready.

{{quote1}}

When investors ask hard questions about your contracts, you need answers fast. That's difficult if your agreements are scattered across email threads, shared drives, and filing systems that only one person fully understands or has access to.

{{quote2}}

Part of what makes due diligence painful is that contract problems often start long before the fundraise.

Teams drafting agreements in different tools, using different templates, negotiating bespoke terms without a consistent baseline: by the time investors ask for a clean picture, there isn't one.

{{quote3}}

Juro addresses this upstream. Self-serve contract templates and workflows mean that business teams create contracts from pre-approved, standardized documents from the start, so your contract portfolio is consistent by default rather than something you have to clean up before a round.

When it comes to diligence itself, Juro's intelligent contract repository brings all your contracts into one place, with AI-powered data extraction that surfaces key clauses, dates, and obligations without manual document review.

Finance teams can run reports on renewal dates, liability caps, and contract values in minutes rather than days. And because Juro embeds in the tools your team already uses, maintaining that repository becomes part of how you work, not a special project you take on before each funding round.

When investors come to review your contracts, you'll be ready.

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Suspendisse varius enim in eros elementum tristique. Duis cursus, mi quis viverra ornare, eros dolor interdum nulla, ut commodo diam libero vitae erat. Aenean faucibus nibh et justo cursus id rutrum lorem imperdiet. Nunc ut sem vitae risus tristique posuere.

Hello. We are Juro Online Limited (known by humans as Juro). Here's a summary of how we protect your data and respect your privacy.

Faisal Al-Alamy, General Counsel at MDLBEAST

Pareen Kohlhaas, Chief Operating Officer at COOP Careers

Bobby Rathore, Senior Legal Counsel at Volt

Bobby Rathore, Senior Legal Counsel at Volt