🇺🇸 1 Boston Place, Suite 2600, MA 02108

🇬🇧 2 Pear Tree Court, London EC1R 0DS

© 2026, Juro. All rights reserved.

🇺🇸 22 Boston Wharf Rd, Boston, MA 02210

🇬🇧 2 Pear Tree Court, London EC1R 0DS

© 2026, Juro. All rights reserved.

Use this free repayment agreement to help outline the terms and conditions for the repayment of a loan or debt.

A repayment agreement is a contract between a lender and a borrower that sets out the terms under which a loan or debt will be repaid. It records the amount owed, the repayment schedule, any applicable interest, and what happens if payments are missed or the borrower defaults.

The agreement applies across a wide range of situations. Two business partners formalizing a loan between them. A company recovering training costs from an employee who leaves early. A creditor and debtor agreeing a structured payment plan rather than immediate full repayment. A property seller providing owner financing directly to the buyer. In each case, the agreement does the same job: it gives both parties a documented, enforceable record of what was promised.

That documentation matters. Without it, both sides are exposed. The lender has limited recourse if payments stop. The borrower has no clear record of the terms they agreed to. For any lending arrangement where meaningful money is at stake, a repayment agreement is not optional.

These two documents overlap significantly, and the terms are often used interchangeably. However, the distinction worth understanding is one of emphasis and timing.

A loan agreement is typically drafted before money changes hands. It governs the full transaction, from disbursement to final repayment, and often includes representations about the borrower's financial position, conditions precedent to advancing funds, and detailed covenants.

Loan agreements tend to be longer and are common in commercial lending contexts where the lender wants comprehensive protection before committing funds.

A repayment agreement tends to come into play when a debt already exists, or where the lending relationship is simpler and less formal. The focus is on documenting the repayment structure rather than governing the initial transaction in detail.

Debt settlement arrangements, inter-company loans, and employee repayment plans are all situations where a repayment agreement is typically the more practical tool.

In practice, many documents used by businesses combine elements of both. A short-form instrument that records the loan amount, the interest rate, and the repayment schedule is a repayment agreement in substance whether or not it is labeled as one.

A related document worth knowing is a promissory note: a simpler, signed promise by the borrower to repay a specific sum by a specific date.

Promissory notes are less detailed than repayment agreements and are typically used for smaller, straightforward lending situations. If your arrangement involves meaningful complexity, a full repayment agreement gives you more protection.

Not all repayment agreements carry the same risk profile, and the distinction between secured and unsecured arrangements should shape how the agreement is drafted.

An unsecured repayment agreement has no collateral behind it. The lender is relying entirely on the borrower's obligation to repay. If the borrower defaults, the lender's remedies are limited to legal action.

This structure is common in smaller inter-company loans, employee repayment arrangements, and personal lending situations where requiring collateral would be impractical or disproportionate.

A secured repayment agreement ties the loan to a specific asset, such as property or equipment. If the borrower defaults, the lender can claim that asset.

Because the lender's risk is lower, secured loans typically carry lower interest rates. They also require more careful drafting, particularly around how the collateral is described and what triggers the lender's right to enforce against it.

If you are structuring a secured lending arrangement, take qualified legal advice on the security documentation alongside the repayment agreement itself. The enforceability of the security interest will depend on how it is documented and, in some jurisdictions, whether it needs to be registered against the relevant asset.

The right level of detail will depend on the size and complexity of the arrangement, but every repayment agreement should address the following:

Parties. Full legal names and addresses of the lender and borrower. In a business context, use the registered entity name, not just a trading name.

Loan amount and disbursement. The principal amount being lent or owed, and when it was or will be advanced.

Interest. Whether interest applies, the rate, how it is calculated, and whether it compounds. An agreement silent on interest can create ambiguity about whether any return was intended. If the loan is genuinely interest-free, say so explicitly.

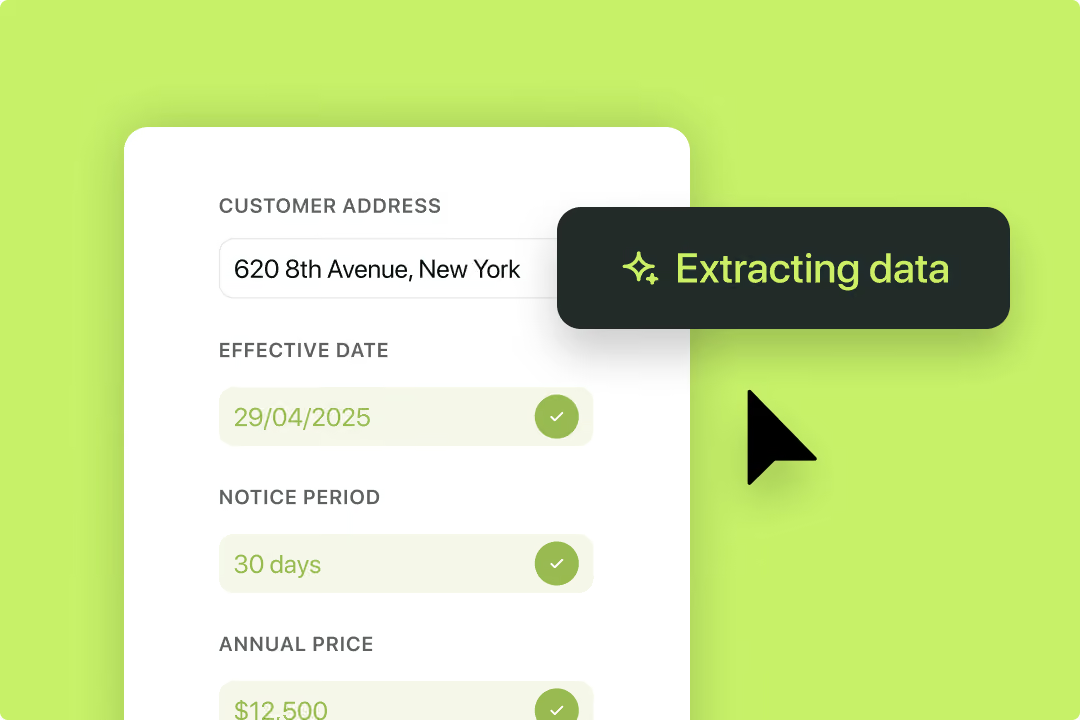

Repayment schedule. The frequency of payments, the amount of each instalment, and the date by which the loan must be fully repaid. If the schedule is variable or milestone-based, set this out explicitly rather than leaving it to be agreed later. A repayment schedule or amortization table appended as an exhibit is often the clearest approach for longer-term or larger loans.

Late payment consequences. What happens if a payment is missed? Many agreements include a grace period before late fees apply, and a separate default threshold that triggers more serious remedies.

Default and acceleration. What constitutes a default, how it is communicated, and whether the full outstanding balance becomes immediately due on default. This clause protects lenders but should be drafted proportionately, with a reasonable cure period built in.

Prepayment rights. Can the borrower repay early? If so, is there a penalty? Lenders earning interest may include a prepayment fee; borrowers should watch for this.

Governing law. Which jurisdiction's law governs the agreement and where disputes will be resolved. For cross-border lending this is especially important. See Juro's guide to contract payment terms for more on structuring payment provisions clearly.

Signatures. Signed by authorized representatives of both parties, with dates. For larger sums, consider whether a witness or notarization is appropriate in your jurisdiction.

When one entity lends to another, whether between group companies, co-founders, or as part of a commercial arrangement, a repayment agreement provides the legal basis for repayment and protects both parties if circumstances change.

When a debtor cannot pay what they owe in full, a creditor may agree to a structured repayment plan rather than immediate recovery action. Documenting that plan in a repayment agreement avoids disputes over what was agreed and provides a clear record if payments later fall behind.

Documenting the repayment obligation at the point of committing to the training, rather than after the employee has already handed in their notice, is always the better approach.

In arrangements where the seller provides financing directly to the buyer, a repayment agreement sets out the loan terms governing that arrangement alongside any transfer documentation.

1. No interest clause. If the loan is genuinely interest-free, state it explicitly. If it is interest-bearing, the rate and calculation method should be precise. Ambiguity here invites disputes.

2. Vague repayment schedules. "Monthly payments" without specifying the amount, the due date, and the total number of payments creates ambiguity. Use a repayment schedule as an exhibit if the arrangement is complex.

3. No default definition. An agreement that says the borrower must repay but does not define what constitutes a default leaves the lender with limited options if payments become irregular without stopping entirely.

4. Missing prepayment terms. If the borrower repays early and the agreement is silent, disputes can arise about whether a prepayment fee was intended. Address this explicitly either way.

5. Unsigned or partially executed agreements. A repayment agreement signed by only one party is not binding. Both parties should retain dated, signed copies.

Verbal agreements to repay a loan are legally binding in many jurisdictions, but they are extremely difficult to enforce in practice.

If the borrower disputes the interest rate, the repayment schedule, or whether a loan existed at all, the lender has almost no recourse beyond their own testimony. Courts can and do enforce verbal contracts, but the burden of proof falls entirely on the party trying to prove what was said.

This matters most in situations where people assume good faith is enough: loans between co-founders, inter-company lending within a group, or advances to employees that are expected to be paid back informally.

The informality feels reasonable at the time and becomes a serious problem when the relationship deteriorates or circumstances change.

A written repayment agreement does not need to be long or complex to be effective. Even a short document recording the amount, the rate, and the repayment schedule, signed by both parties, is vastly more enforceable than a conversation.

Repayment agreements are signed with a set schedule in mind, but commercial and personal circumstances change:

What happens to the repayment agreement when the original terms are no longer workable?

The starting point is the amendment clause in the original agreement.

Most repayment agreements require any contract variation to be agreed in writing by both parties.

An informal email exchange or a verbal agreement to delay payments is not a reliable substitute for a proper amendment, and in a dispute, the court will generally look at the signed document rather than subsequent correspondence.

If the parties agree to change the repayment schedule, the interest rate, or the total amount owed, that change should be documented in a written amendment referencing the original agreement, signed by both parties, and stored alongside it.

For a straightforward extension of time, a simple contract addendum recording the new schedule is usually sufficient. For more significant changes, including any reduction in the principal, it is worth considering whether the amendment needs to be drafted carefully to avoid unintended tax or legal consequences.

Juro's guide to contract amendments covers the mechanics of how to do this correctly.

The practical risk in not documenting changes is that the lender retains the right to enforce the original terms even if they verbally agreed to a more lenient arrangement. Equally, the borrower has no documented evidence that additional time was granted if the lender later changes their position.

A single repayment agreement is straightforward to track manually.

The real challenge emerges for finance and HR teams managing repayment arrangements in higher quantities: training cost recovery agreements across a large workforce, structured debt repayment plans with multiple counterparties, or inter-company loan arrangements across a corporate group.

SaleCycle, a behavioral marketing company with over 650 contracts per year and a one-person legal team, experienced this problem before adopting Juro. Contracts were bouncing between five different tools with no single source of truth.

After implementing Juro, their General Counsel recovered around nine working days per month that had previously been consumed by contract administration, without having to hire additional headcount.

For repayment agreements specifically, the practical gains come from having the agreement, the payment schedule, and any amendments stored in a searchable, centralized contract repository where key dates are tracked and surfaced automatically.

Juro makes it possible to set reminders for contract milestones and default trigger dates, and to surface the original agreement in seconds when a question arises.

Finance and HR teams that create repayment agreements regularly can also benefit from Juro's automated contract templates. Legal defines the approved terms and the fields that can be varied, and the business team generates an agreement without needing legal involvement for every instance.

To see how that works in practice, book a demo or join the Juro community to hear how other teams structure their financial agreement workflows.

Juro is the #1-rated contract platform globally for speed of implementation.

Hello. We are Juro Online Limited (known by humans as Juro). Here's a summary of how we protect your data and respect your privacy.